Home Insurance is a way to safeguard the most valuable assets – your home and your belongings. With this insurance, you can protect your house against unexpected events, such as accidents, natural disasters, theft, and vandalism.

This insurance will financially cover the losses so that you don’t have to continuously worry about your potential home-related losses.

With comprehensive coverage, you can experience a stress-free tomorrow.

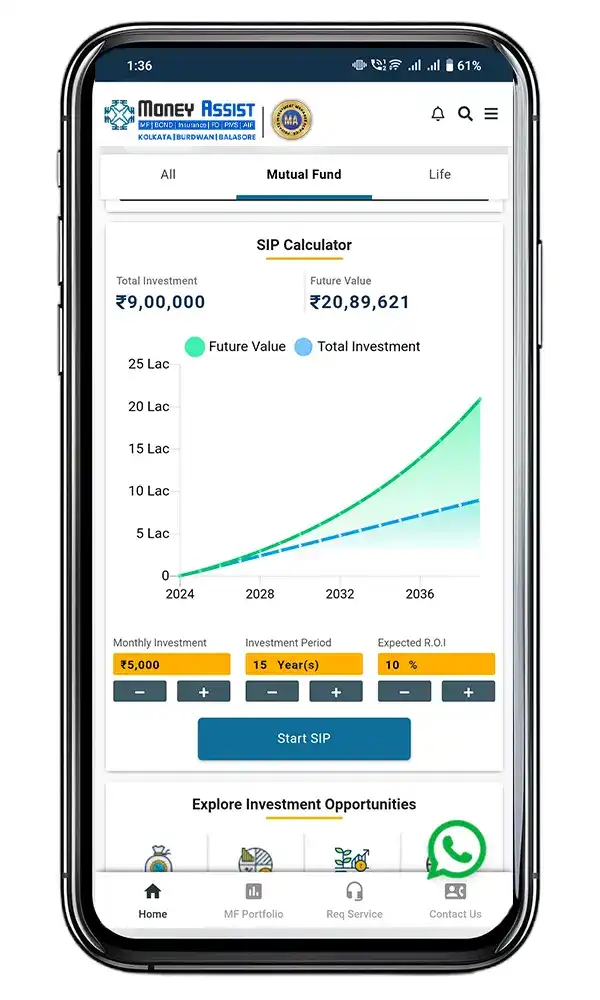

Finance is an asset. While you work to accumulate it, we work to grow it. Be it for your retirement or to achieve your dream goal, or be it to make your decendants financially secure, we ensure that your wealth is protected across generations.

Home Insurance policy offers financial protection for the constants and structure of the house in any event of physical destruction or damage that is caused to the property by any unavoidable perils. The damage can be both man-made or due to natural calamities. It is highly cost effective and offers cover for damages to the building, the possessions and more at a lower premium rate.

Coverage: Offers minimal coverage. It normally covers specific perils inclusing fire, theft, and some natural disaster coverage.

Popularity: This form is not in use because it lacks protection. Most homeowners need personal property and liability to feel secure.

Coverage: This policy also gives more coverage in regard to HO-1, although including further risks like falling objects or water damage from plumbing.

Scope: A bit more sophisticated than simple coverage but not quite comprehensive.

Coverage: Every peril is insured under this most popular kind, besides the ones that are specifically identified as excluded from the policy.

Structure vs. Contents: The structure of the house is insured in “all perils,” while personal belongings are insured in “named perils.”

Coverage: Designed specifically for the tenant, covering personal property and liability but not the structure.

Target Market: Ideal for policyholders that need coverage for their personal items.

Coverage: The most comprehensible policy offered, which insures your home and personal property against everything unless listed in the policy as an exclusion.

Price: More expensive than other policies because it provides comprehensive coverage.

Coverage: Written for the owner of a condo and their needs, both personal property within the unit, as well as the interior walls and any improvements and betterments made to the unit.

Association Coverage:

Written for those who purchase coverage in tandem with a master policy carried by a condo association. The master covers only the exterior of the building and the common areas.

Coverage: Written for mobile or manufactured homeowners. Offers all the same protection as HO-3 but with special considerations for the unique risks mobile homes face.

Special Considerations:

Written for those who own older homes and are looking to cover the unique risks involved with the ownership.

Coverage: Intended for older homes, where the amount to replace them is greater than their market value. It covers actual cash value rather than replacement cost.

Suitability: Often used for historic or architecturally significant homes.

Coverage: This one is designed for people who own a property that they don’t live in, which provides coverage for the building, liability as well as loss of revenue regarding rental money, in case your tenants can no longer live there.

Extended Coverage: May cover landlord’s personal property used to preserve the rental-e.g., appliances or lawn equipment.

Coverage: For occupiers, the insurance covers personal property, personal liability, and additional living expenses if the residence becomes unlivable.

Affordability: Typically more affordable since insurance does not extend to the structure of the building.

Coverage: Covers in cases where there is a flood incident, which generally is not part of a standard policy to cover homeowners.

Requirement: Typically required by many lenders in higher-risk flood areas; available to homebuyers separately through the NFIP or from the private market.

Coverage: Provides protection against damages to your home and possessions resulting from an earthquake, which a typical homeowner’s policy does not cover.

Optional Add-On: An endorsement to a standard policy or as a stand-alone policy.

Coverage: Provides protection in the event of loss from windstorms, hurricanes, and tornadoes, that would have been excluded from the standard policy covers in the event of high-risk zones.

Requirement: Imposed mostly in the hurricane-prone coastal areas.

Coverage: Serves as one excess liability insurance policy over one’s homeowners or auto insurance policy.

Purpose: Provides protection for some claims, or lawsuits, that rise above the primary policy limits.

Coverage: It enables repair or replacement of major home systems and appliances against normal wear and tear, which generally are not covered in routine homeowner insurance policies.

Optional Service: It is not usually marketed with insurance; rather it is in the nature of a service contract.

The benefits of investing in Home Insurance are–

Homeowners willing to reduce stress and keep the property protected from man-made and natural calamities can purchase Home Insurance Plans.

Enquire Now

Start by evaluating your needs and value of your house. Then, you can research the home insurance policies that are available in the market. This is essential to find the right one to fit your goals or objectives. You can also take help of an expert to help you invest in the right insurance policy.

Contact Us

Partnering with us can help you get expert guidance and unparalleled support for choosing the right insurance policy. We not only offer personalised assistance and guidance but also deliver exceptional solutions with our extensive knowledge and expertise.

Yes, the home insurance policies are typically renewable every year. So, you can renew them annually with the same existing plan or a new one.

There are many factors that play a major role in deciding the premium of your home insurance. These are – your security features, location of the house, age of the property, and past claims.

Yes, in case your house becomes inhabitable due to the damage, then your temporary living expenses will be covered by the home insurance policy.

It depends from one policy to another policy. Most of the time, standard policies do not include coverage for the flood damage or earthquake damage. But, you can check out the special plans if you want.